ET Drone Home

Adulting Abby Wilson January 22, 2025

Adulting Abby Wilson January 22, 2025

If you've been shopping around for homeowners' insurance lately, you might have noticed that insurance companies are getting a bit pickier, especially when it comes to certain features of your home like the roof and electrical wiring. So, what's the deal? Let's dive into why these specific areas are under the microscope.

The Roof Over Your Head

First up, let's talk about roofs. They are the first line of defense against the elements, and insurance companies know it. With the increase in extreme weather events—think hurricanes, heavy snow, and hailstorms—roofs are taking a beating more than ever. Insurers are now paying extra attention to the age and condition of your roof, and they may even send drones over your house to verify its condition after you've moved in. If your roof is old or in poor shape, this is a higher risk for claims.

We spoke to an insurance agent recently who said, if you've got a roof that's more than 15 years old in Pennsylvania, good luck finding a home owner's insurance policy when you're trying to buy. As a buyer, you might be required you to replace or repair your roof before they’ll insure your home, they could charge higher premiums, or you could have a specific timeline by which you need to have your roof replaced in order to maintain coverage. For sellers, your real estate advisor might encourage you to consider replacing the roof before selling if your roof is more than 20 years old. We know it's a huge investment, and we also know it will save you time, money, and stress while your property is on the market and under contract.

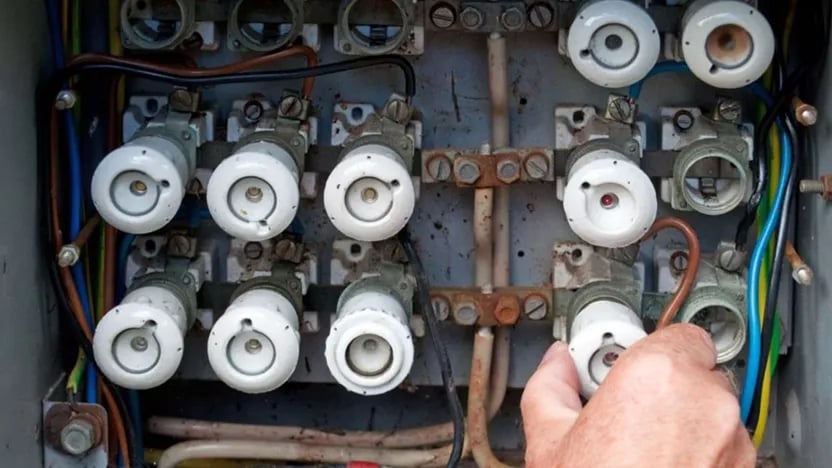

The Knob-and-Tube Conundrum

Now, onto knob-and-tube wiring. If you live in an older home, you might have this type of wiring, which was common in homes built before the 1950s. While it was state-of-the-art back in the day, it doesn't meet today's safety standards, and insurance companies rarely want anything to do with it! This type of wiring poses a fire risk, the insulation can degrade over time, and it simply wasn't designed to handle the electrical loads of modern appliances. Things get especially dangerous when knob and tube wiring is spliced or joined to newer, modern wiring. Like the roof scenario, insurers might require you to upgrade your electrical system before offering coverage, increase your rates to offset the risk, or place a timeframe during which you need to make repairs after closing.

Why the Crackdown?

It all boils down to risk management. With the potential for costly claims due to roof damage or electrical fires, insurers are trying to protect themselves from avoidable big payouts. By being more selective, they aim to ensure they can cover claims without breaking the bank.

What Can You Do?

If you're dealing with these issues, don't worry—there are steps you can take. Sellers: consider getting a pre-list inspection and make necessary repairs or replacements before you list the property. Remember - real estate surprises are rarely - if ever - good surprises! Know what you might be getting into before you've found a buyer who'd like to make your home their own. For knob-and-tube wiring, same advice. Get it inspected, know what you're dealing with, and - if you ask us - just get rid of the knob and tube. Not only can these improvements help you secure and maintain home owners' insurance, but they can also increase your home's safety and value.

We’re in the Experience Business, Not the Transaction Business “It is not enough that we build products that function, that are understandable and usable, we also need to build products that bring joy and excitement, pleasure and fun, and, yes, beauty to people’s lives.” – Don Norman, Author, The Design of Everyday Things